I posted an article a few days ago that examined the theoretical relationship between interest rates and purchasing power. The calculations beg the question “are interest rates and Hawaii home prices actually connected?”

Logic says “of course!”, the data suggests “not so much!”

Let’s assume a 20 percent down payment, market loan fees (points), and monthly payments of 35 percent of a household’s gross income.

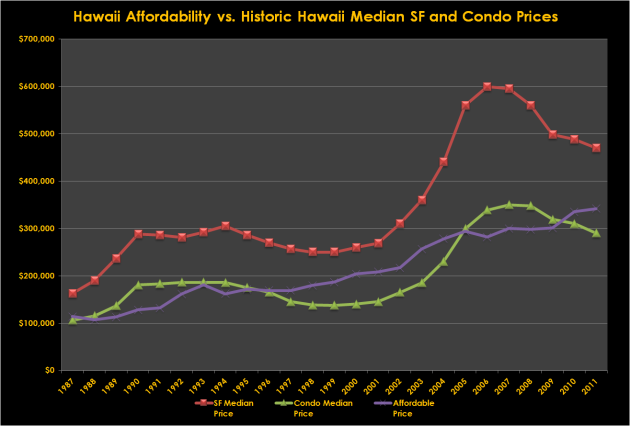

The following chart shows State of Hawaii median income, condominium median prices, single family median prices, and national average interest rates for 30-year mortgages from 1987 through 2011 (the latest year for which all data points are available).

Sources: U.S. Census Bureau, Freddie Mac, Hawaii State Data Book, and Chris Ponsar, MAI

Based upon the income and interest rates shown, the median Hawaii family could afford a monthly payment of $1,021 in 1987, and $1,722 in 2011. These payments equate to affordable home prices of $114,370 in 1987, and $341,898 in 2011. (A pretty hefty increase in purchasing power, driven largely by lower interest rates)

Lets see how the figures track with historic price fluctuations in the Hawaii residential real estate market.

The red and green trendlines track single family and condominium prices in the study period–as shown, condos and single family home prices track pretty well.

How about affordability (the purple trendline) based on interest rates ?

The long term trend is clearly positive for all variables, with affordable price, condo price, and single family price all being about 3x higher in 2011 than they were in 1987.

But that’s not the question most folks are asking. The market participants I talk to are generally trying to answer the question “If interest rates go up (this year, or next year), will prices go down (this year, or next year)?” Is it a causal relationship?

What do you think? Personally, beyond long term growth, I don’t see a strong relationship in the data, and neither is a solid correlation revealed in geeky statistical analyses.

Why isn’t the correlation better?

Higher interest rates do equate to lower affordability for a particular household, but why doesn’t that relationship translate well into median prices?

A few suggestions:

- Median prices are not the best way to measure market trends–overall dollar volume and the raw number of sales may provide more insight (and material for a future article)

- Hawaii’s population continues to grow faster than new housing units are developed–fundamental demand grows incrementally in both good times and bad. (Which explains the overall upward trend in prices, but not the ups and downs in particular years)

- When monthly payments go up, families still need shelter. For those families contemplating a home purchase, spending on discretionary items will likely suffer first (say vacations or luxury items)–these spending habit adjustments allow families to absorb a certain amount of extra monthly payment caused by increased interest rates.

- When prices start to decline, sellers may opt not to put their home on the market. Financially stable homeowners can afford to “hold out” for their desired price, which restricts supply, and in turn has a stabilizing effect on prices.

Frankly, when I began researching the data for this article, I expected to see a pretty reasonable relationship between affordability and median prices–instead, we see that from the perspective of a current homeowner, prices appear not to fluctuate on a “dollar for dollar” basis with interest rates. From an appraiser/appraisal perspective, it is imperative to observe how the market reacts to the rising rates that are currently anticipated, not just automatically assume lower prices if interest rates rise.

Comments and/or Questions? Please leave them in the comments section below–I’d be happy to clarify or expand.

Aloha, Chris

Recent Comments