Land Value via the Income Approach – A Quick Primer

July 22, 2013

If you’re generally familiar with real estate appraisal, you are no doubt aware that the sales comparison approach is the preferred method of valuing land in most situations.

That said, there are other techniques that can be developed: Market Extraction, Allocation, Land Residual, Ground Rent Capitalization, and Discounted Cash Flow Analysis.

The last three procedures in that list are income capitalization techniques–they are the focus of this article.

Subdivisions are often valued via the income approach.

Subdivisions are often valued via the income approach.

Ground Rent Capitalization

Due to the large amount of leasehold land in Hawaii, local appraisers frequently employ this technique to convert ground lease rents into land values.

In appraisal school, one of the first formulas taught is: Income / Rate = Value ( I / R = V )

Here is an example of how it works:

As shown, a property’s annual income can be converted to a land value if a capitalization rate, or “rate of return” as it is commonly called in Hawaii, can be derived from the market. In this example, if an eight percent (8.0%) rate of return was applied to a ground rent of $50,000 per year, the indicated land value would be $625,000.

Land Residual

Similar to the Ground Rent Capitalization technique described above, this method converts the allocated portion of a property’s income that is attributable to the land, and again divides it by a land capitalization rate that is market derived. Most often, this method is employed when testing the feasibility of alternative uses in highest and best use analyses.

The key difference between this technique and the one above is that income for an improved property is typically the starting point, and it must be segmented (with market support) into the income attributable to land (IL) and income attributable to the building (IB).

The following chart is an example of the Land Residual technique used for Highest and Best Use testing purposes:

(Note: In my experience in Hawaii, this method is used so infrequently for market value purposes that the term “Land Residual” is most often meant by appraisers to describe Yield Capitalization/DCF/Subdivision/Development Analyses–described below)

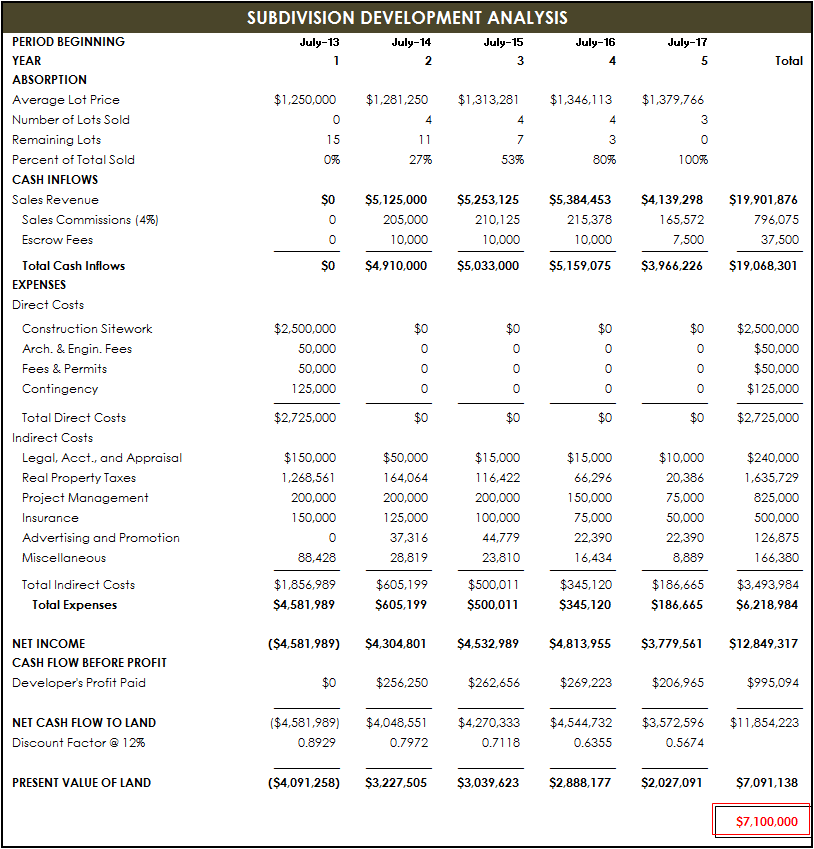

Discounted Cash Flow Analysis / Subdivision Development Analysis

Yield Capitalization can also be used to value land, it is sometimes referred to as one of the following techniques:

- Discounted Cash Flow Analysis

- Subdivision Analysis

- Development Analysis

- Subdivision Development Analysis

- Yield Capitalization

- Land Residual (Hawaii)

In this technique, gross sale prices are estimated and costs (such as construction, management, or developer’s profit) are deducted to arrive at net income. This net income is then discounted to a present value estimate for the underlying land.

An example of a Subdivision Development Analysis is shown below:

Comments and/or Questions? Please leave them in the comments section below–I’d be happy to clarify or expand.

Aloha, Chris

Recent Comments